Original from: Siemens Healthineers

Siemens Healthineers AG today announces its results for the fourth quarter of fiscal year 2025 ended September 30, 2025, and the full fiscal year 2025.

Fiscal Year 2025

Īż Very good equipment book-to-bill ratio of 1.14

Īż Strong comparable revenue growth of 5.9%

Īż Adjusted EBIT margin of 16.5%, 0.8 percentage points above prior year despite higher tariffs; adjusted EBIT up to just under Ć3.9 billion

Īż Adjusted basic earnings per share of Ć2.39

Īż Free cash flow of around Ć2.7 billion, clearly above prior year

Īż Proposed dividend of Ć1.00 per share (prior year: Ć0.95)

Q4 Fiscal Year 2025

Īż Very good equipment book-to-bill ratio of 1.12

Īż Comparable revenue growth of 3.7%

Īż Imaging comparable revenue growth of 6.5%; adjusted EBIT margin of 20.6%

Īż Diagnostics comparable revenue flat (-0.3%); adjusted EBIT margin of 7.5%

Īż Varian comparable revenue up 1.4% against very strong prior-year quarters; adjusted EBIT margin of 19.7%

Īż Advanced Therapies comparable revenue growth of 3.8%; adjusted EBIT margin of 17.5%

Īż Overall adjusted EBIT margin of 17.4%, slightly under the prior-year quarter due to higher tariffs

Īż Free cash flow of around Ć860 million

Īż Adjusted basic earnings per share of Ć0.68, slightly above prior-year quarter

Outlook for Fiscal Year 2026

For fiscal year 2026, we expect comparable revenue growth of between 5% to 6% compared with fiscal year 2025. We expect adjusted basic earnings per share to be between Ć2.20 and Ć2.40.

Bernd Montag, CEO of Siemens Healthineers AG:

Ī▒We have closed another successful year, despite a challenging environment. Following this achievement, we are raising our proposed dividend. We have a solid foundation for our next strategy phase.Ī░

Business Development Q4

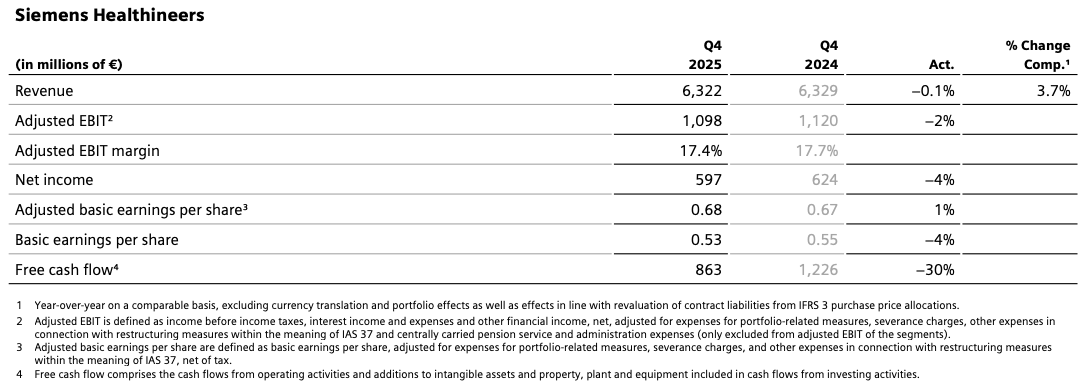

Revenue rose by 3.7% on a comparable basis in the fourth quarter of fiscal year 2025 to around Ć6.3 billion. This growth was attributable in particular to strong revenue development in the Imaging segment.

From a geographical perspective, the Americas region showed strong comparable revenue growth. Revenue in the Asia Pacific Japan region grew moderately and in EMEA slightly, while revenue in the China region declined by a low-single-digit percentage range.

Equipment order intake in the fourth quarter clearly exceeded equipment revenue. The equipment book-to-bill ratio was a very good 1.12.

In the fourth quarter, adjusted EBIT of almost Ć1.1 billion was slightly below the prior-year period. This resulted in an adjusted EBIT margin of 17.4%, also slightly below the prior-year quarter. Higher tariffs had a negative effect in all segments. This was offset by contributions from revenue development as well as cost reductions in connection with the transformation program of the Diagnostics business.

Net income was Ć597 million, down 4% from the prior-year period. The tax rate was 23%, below the tax rate of the prior-year quarter.

Adjusted basic earnings per share of Ć0.68 were slightly above the prior-year quarter. The lower tax rate as well as higher earnings from the operating business more than compensated for lower financial income, net and higher tariffs.

Free cash flow of Ć863 million was below the very strong prior-year quarter.

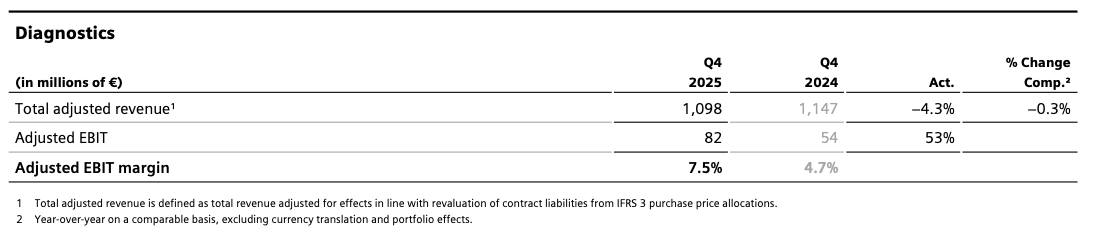

In the Diagnostics segment, revenue in the fourth quarter was flat on a comparable basis (-0.3%). Revenue was just under Ć1.1 billion.

While Diagnostics revenue grew very strongly in the Asia Pacific Japan region and moderately in the EMEA region, the segment showed a slight revenue decline in the Americas region. In the China region, the low double-digit-percentage revenue decline was attributable in particular to centralized volume-based public procurement.

The segmentĪ»s adjusted EBIT margin of 7.5% was clearly above the prior-year quarter level, mainly due to cost reductions in connection with the transformation program. The prior-year quarter was negatively impacted by effects relating to prior periods.

Reconciliation to consolidated financial statements

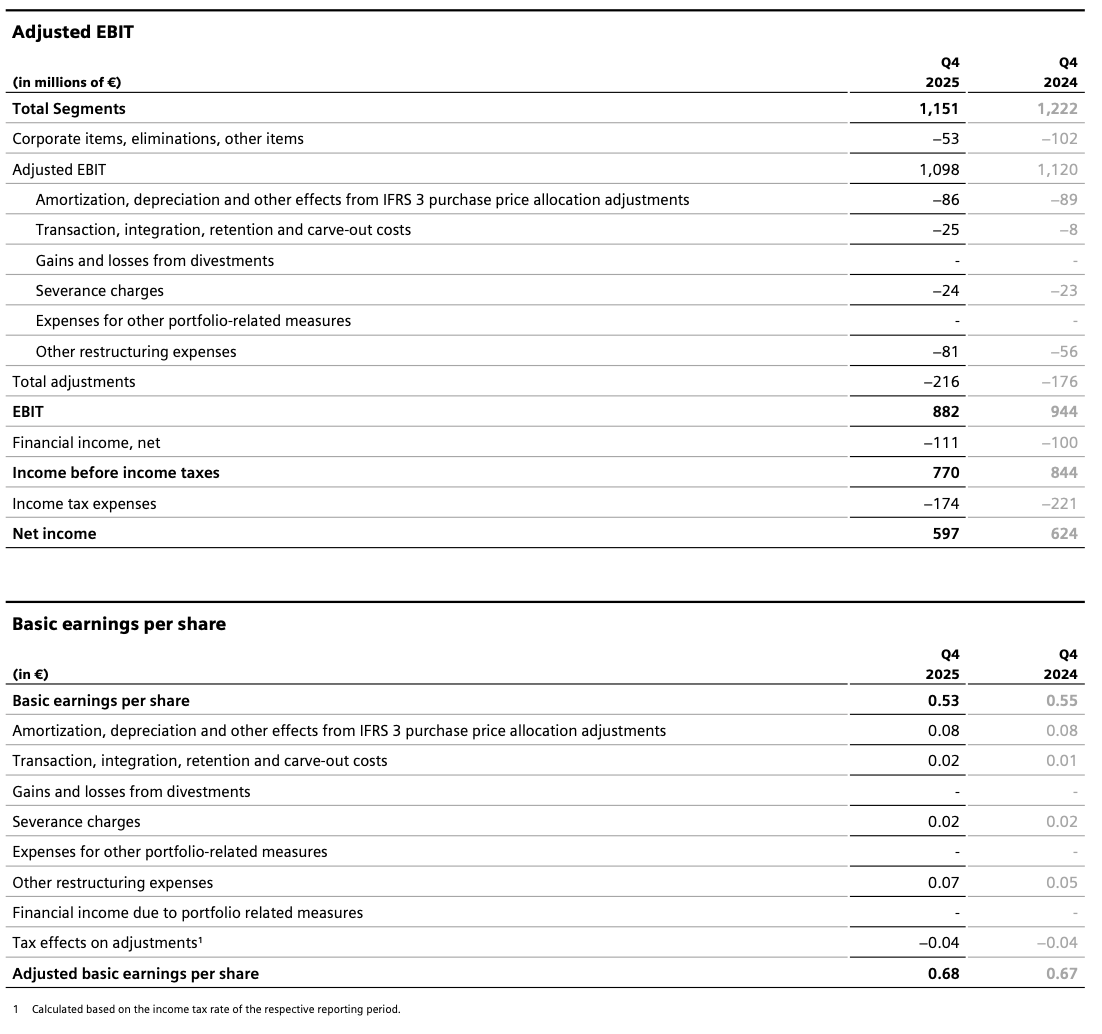

Other restructuring expenses rose by Ć25 million to Ć81 million. In particular, this included higher expenses in connection with the transformation of the Diagnostics business.

Financial income, net declined by Ć12 million to -Ć111 million.

Net income declined from the prior-year period by 4% to Ć597 million. The tax rate was 23%, below the 26% tax rate of the prior-year quarter.

Adjusted basic earnings per share of Ć0.68 were slightly above the prior-year figure of Ć0.67. The positive effect of a lower tax rate as well as increased earnings contributions from the operating business more than compensated for lower financial income, net and higher tariffs. Adjustments increased over the prior year, mainly due to higher other restructuring expenses in connection with the transformation of the Diagnostics business.

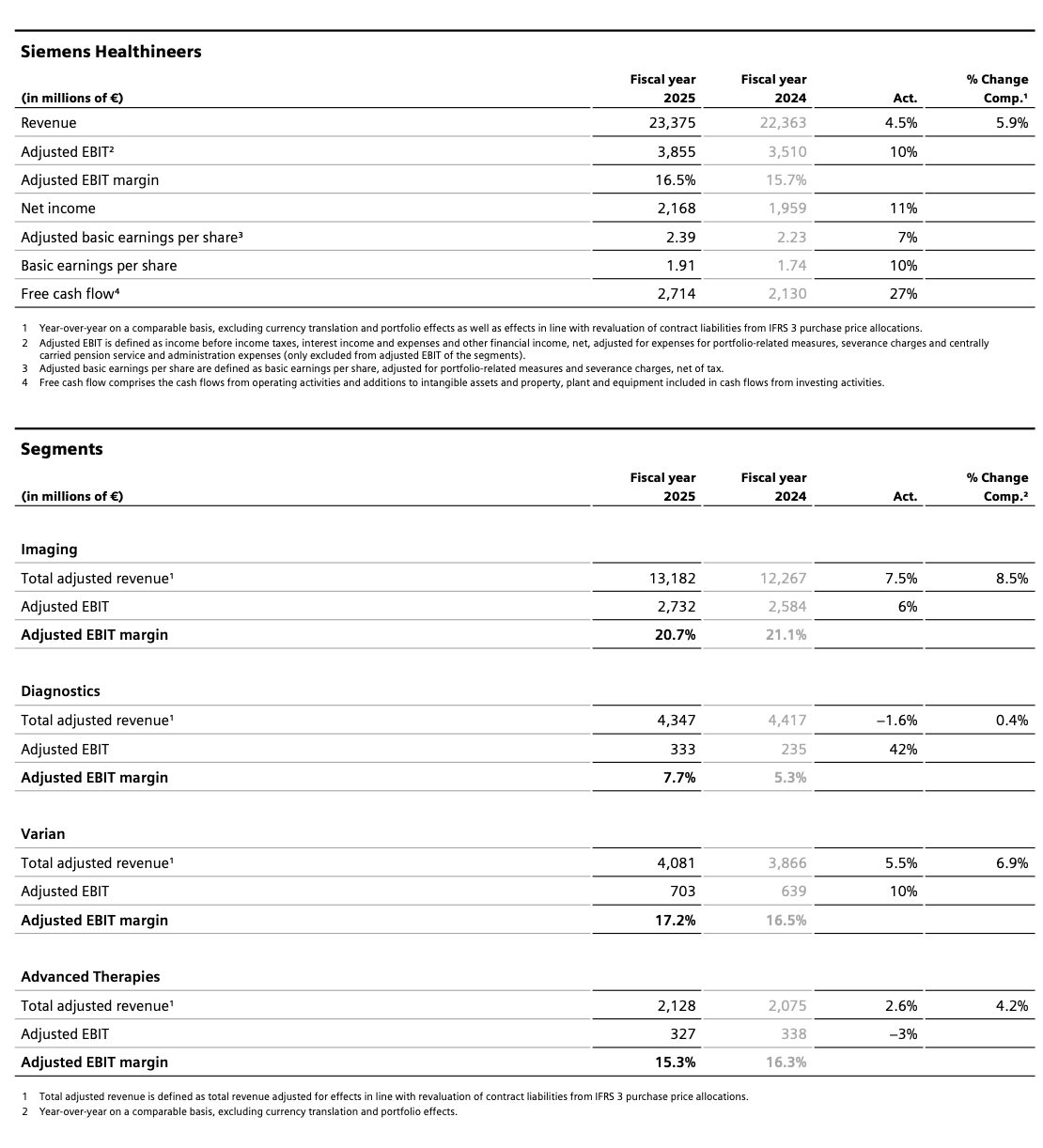

Revenue rose 5.9% on a comparable basis in fiscal year 2025. This was mainly due to very strong growth in the Imaging segment and strong revenue development at Varian.

From a geographical perspective, the significant year-on-year revenue development in the Americas region contributed most clearly to growth. In the Asia Pacific Japan region, revenue rose strongly and, in the EMEA region, slightly.

Meanwhile the China region showed a slight revenue decline.

Nominal revenue was Ć23,375 million.

The equipment book-to-bill ratio was a very good 1.14, above the prior-year figure of 1.11.

Adjusted EBIT rose in fiscal year 2025 to almost Ć3.9 billion. The adjusted EBIT margin increased by around 80 basis points from the prior year to 16.5%. Strong revenue development as well as cost reductions in connection with the transformation program in the Diagnostics business had a positive effect. Higher tariffs, which had an impact on all segments, had a negative effect.

Adjusted EBIT margin in the Imaging segment was 20.7%, below the prior-year level. Earnings contributions from revenue development were impacted by higher tariffs. In the Diagnostics segment, the adjusted EBIT margin of 7.7% was clearly above the prior-year level. This was mainly driven by cost reductions in connection with the transformation program.

Against the backdrop of strong revenue development, adjusted EBIT margin in the Varian segment was 17.2%, above the prior year. The adjusted EBIT margin in the Advanced Therapies segment was 15.3%, below the prior-year level. Earnings contributions from revenue growth were impacted by higher tariffs.

Net income was just under Ć2.2 billion, up 11% from the prior year. In both fiscal years, there were restructuring expenses in the low triple-digit-million range in connection with the transformation of the Diagnostics business.

The tax rate was around 24%, above the prior-year level.

Adjusted basic earnings per share of Ć2.39 were clearly higher than the prior-year figure of Ć2.23. Adjusted for currency effects, adjusted basic earnings per share rose by around 9%. Increased earnings contributions from the operating business more than compensated for higher tariffs compared with the prior year, and higher tax expenses.

At around Ć2.7 billion, free cash flow was clearly higher than in the prior year. The main reason for this was higher cash flow from operating activities.

Outlook

For fiscal year 2026, we expect comparable revenue growth of between 5% to 6% over fiscal year 2025.

Adjusted basic earnings per share are expected in the range of Ć2.20 and Ć2.40.

The outlook is based on several assumptions. This includes assumptions about exchange rate developments, which currently lead to a significant negative currency effect on the expected adjusted basic earnings per share for fiscal year 2026 compared with fiscal year 2025. Furthermore, this outlook excludes potential portfolio measures. In addition, the outlook is based on the assumption that developments related to wars and conflicts will not have a material impact on our business activities. The outlook is based on the number of shares outstanding at the end of fiscal year 2025.

This outlook is based on the assumption that the current macroeconomic environment, including the interest rate level, will remain largely unchanged. Further charges from legal, tax and regulatory issues and framework conditions, for example changes in the level of tariffs and the resilience of our supply chains, are excluded.

Source: Siemens Healthineers successfully closes 2025 fiscal year in challenging environment